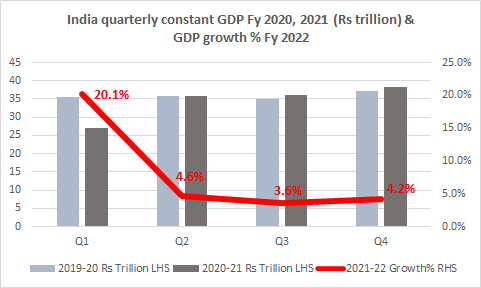

Fifteen months down the road to economic recovery, the economy is still limping back to the normal circa 2019-20. GDP in the first quarter of the current fiscal year (April to June fiscal year 2021-22) at INR 32.4 trillion (constant terms) is 20.1 percent higher than the same quarter last year- that’s the good news. But it does still remain 9 percent below the INR 35.7 trillion in the Q1 two years ago in 2019-20. Nevertheless, the trend is becoming brighter with each passing month that the stranglehold of the pandemic ebbs.

Growth — Here today, gone tomorrow, the “base effect” smoke and mirrors

However, it is good to remember that recovery from a continuing external shock, like the pandemic, is quite different from growing GDP in real terms, past levels achieved in more normal times, as in 2019-20. Graduating from the “recovery phase” to the “rehabilitation phase” which precedes the “development-all-engines-firing” phase means clocking an average growth at 8.5 percent, to cross the GDP level of INR 145.7 trillion (constant terms) in 2019-20.

This seems like a cakewalk, with the economy growing at 20.1 percent in Q1 over the same quarter last year. But as the graph below illustrates, it is anything but. GDP levels in quarters 2 to 4 last year, were not only marginally better than in 2019-20 but also significantly higher than in Q1, which represents the economy at the bottom of the V, U or L shaped curve. The red line tracing quarterly growth this year versus the previous year’s quarter is consequently likely to dip sharply downwards from 20.1 percent in Q1 to growth levels between 4 to 5 percent in succeeding quarters, ending the year with an average growth between 8.5 to 9.5 percent.

Sample this factoid. Despite the 20.1 percent growth in Q1 this year, the value added in real terms (INR 32.9 trillion) is 17 percent below the value added in the preceding quarter of last year (INR 39 trillion Q4 Fiscal 2020-21). The RBI predicts growth to be 9.5 percent this year which, if achieved, would set the stage for India to enter the “rehabilitation” phase of economic reconstruction, albeit with large dollops of social protection.

This is when we will be testing the sinews of the economy — our capacity to enhance productive investment, our ability to tease out better output from existing investments and our ability to invest in or buy research and development advances to lift the Indian economy to the next-gen level. These will be salient issues for Fiscal 2022–23; not this year, which is more about stabilising the economy. Key in this endeavor is controlling consumer inflation, which is coasting along at the upper bound level of 6 percent.

Diversified sources of value addition and markets to the rescue

We must count our blessings that nature has been benign during the pandemic. Agriculture, which did well last year to grow at 3.6 percent annually over 2019-20 levels, continues to be the source of growth and jobs with a 4.5 percent growth in Q1 of this year over the same quarter last year. This happy situation might change over the next quarter if the Kharif crop gets affected by delayed sowing, due to the disturbed rainfall pattern this summer.

Another saviour is exports, which increased 7.7 percent this quarter over the same quarter last year. Both agriculture and exports highlight the advantages of a diversified economy and diversified markets, in riding out a domestic downturn. Had agriculture been more dynamic and responsive to the opportunities in international markets, rather than primarily focused on subsidy-fuelled cereal production for domestic consumption, the positive outcome for the economy, jobs and incomes could have been even more substantial.

Indifferent investment outcomes

Investment metrics are a good predictor for growth. Sadly, investment levels continue to be indifferent at INR 10.2 trillion (public and private) in Q1 Fy2021-22. Though it was substantially higher than last year in the same quarter, it remains 17.1 percent percent lower that the INR 12.33 trillion (constant terms) achieved in 2019-20 in the same quarter.

The INR 2.1 trillion drop in investment level evidences that the INR 7 to 8 trillion in extra liquidity infused by the Reserve Bank of India was not channeled into productive real assets. Instead, it seems to have served to enhance demand for consumer durable via easy credit facilities to “bankable” middle class consumers or companies, funded MUDRA loans to unemployed youth and small entrepreneurs, which have NPA levels in the low double digits or financed investments in stock markets keeping them at rich levels relative to average yield. This is unsurprising. With business capacity utilisation levels low, at around 70 percent, only the foolhardy or those unaffected by the pandemic, would commit funds to clunky capital investments.

Deleveraging the public sector

More heartening is the government’s recent initiative to monetise operational assets of the public sector by leasing them on a long-term basis to private investors. This will substitute private for public sector capital and provide an exit option for public sector capital.

The twelfth plan ending in 2017 had targeted nearly one half of investment coming from the private sector, which proved unfounded. Consequently, against a targeted investment level in infrastructure of 9 percent of GDP in the terminal year of the plan, the actual average results were just 5.8 percent of GDP.

Over the past decade, investment peaked at 34 percent of GDP in 2011-12 before starting a secular decline across the private and public sectors to 32.2 percent of GDP in 2018-19, 30 percent of GDP in 2019-20 and 28 percent of GDP in 2020-21 with a corresponding negative impact on growth over the last nine quarters.

COMPETING PRIORITIES

With tax levels to GDP stagnant, government budgets spend far less on social sector support than is the norm across East Asia or Europe. One of the lessons from the pandemic is that paying short shrift to health infrastructure and services can have serious negative economic consequences. The quality of publicly provided or supported education in India is well documented to be far from adequate for imparting life-skills or preparing aspiring youth for productive jobs. Sharp increases in outlays for the provision of social services are a priority.

Delinking government from being the major investor in infrastructure is, consequently, urgently necessary, as was conceived in the post 2008-09 western financial crisis period.

The July 2021 Union government accounts outturns supports this hypothesis of the need to converge government finances in areas where private investments might not easily flow and to vacate the areas where private investment feels comfortable investing. Investment expenditure by July 2021 was just 23.2 percent of the budgeted INR 5.5 trillion (16 percent of total budgeted expenditure), against an average spend of 28.8 percent for all expenditure. Interest payments on outstanding debt accounts for around 23 percent of all expenditure.

With increased fiscal deficits, the stress on resources is obvious. Leasing out operational assets, listed in the national Monetisation Pipeline, and continuance of the disinvestment programme can add fiscal space of 1 percent of GDP (INR 2 trillion) equal to around 6 percent of the budgeted Union expenditure.

The international experience and our own limited privatisation experience (1999-2003), illustrates that private investment, operating under arms-length, professional anti-trust and environmental regulatory constraints, is an efficient public choice for manufacturing industrial products and public service delivery.

Using the public sector as a “Trojan horse” to overcome pesky regulatory constraints for speedier project implementation – a convenient start-up mode- which sells out, once the project is up and running, to private investors, is a workable second-best option. But the long-term solution, lies in governance and regulatory reform to facilitate direct private investment in infrastructure.

Substituting public capital, employed in business ventures, with private capital; conserving public capital for social sector investments; and pulling-out-all-the-stops in making business and environmental regulations efficient and least-cost is the trifecta of initiatives demanding attention.

Adapted from the author’s opinion piece in https://www.orfonline.org/programme/economy-and-growth/ September 2, 2021

Thank you Dr. Nitin Desai for pointing out the data snafu in paragraph one. My words mixed up the comparison of this years Q1 GDP levels with same quarter last year and the year before. Sorry readers! Now corrected.